Photo by Kelly Sikkema on Unsplash

In case you hear a faint whimpering noise in the distance, that’s the sound of a neoliberal who has just sensed the word “taxes” in the air.

Sure, getting dollar bills plucked from your overworked to the point of barely functioning fingers feels painful, but when you remember that money is supposed to be a medium of exchange for goods and services, it seems the agony experienced may be from the lack of return on the forced income trim, not the cash cut itself.

Taxes pay for schools, school lunches, libraries, roads, scientific research, Medicare, Medicaid, Social Security, food safety inspections, and multitudes of other useful and productive public programs. They could also pay for a universal healthcare system to fix your twisted dangly hand hot dogs that are desperate to hold on to any and all monies because the U.S. has a social safety net with the strength of a soggy saltine, but they don’t.

The National Priorities Project provides a tool which shows the breakdown of where your federal taxes were spent each year. In 2024, the average taxpayer in the United States paid $17,766 in federal taxes with $3,707.81 going to war and weapons and $3,452.73 put toward the national debt. That’s a little over 40% of the average U.S. taxpayer’s federal taxes either blowing up people and the planet or trying to dig the country out of the ever-deepening hole it’s in which is often escalated by tax cuts and its continued spend on violence.

Something to think on as we delve into how the federal taxes you owe are calculated.

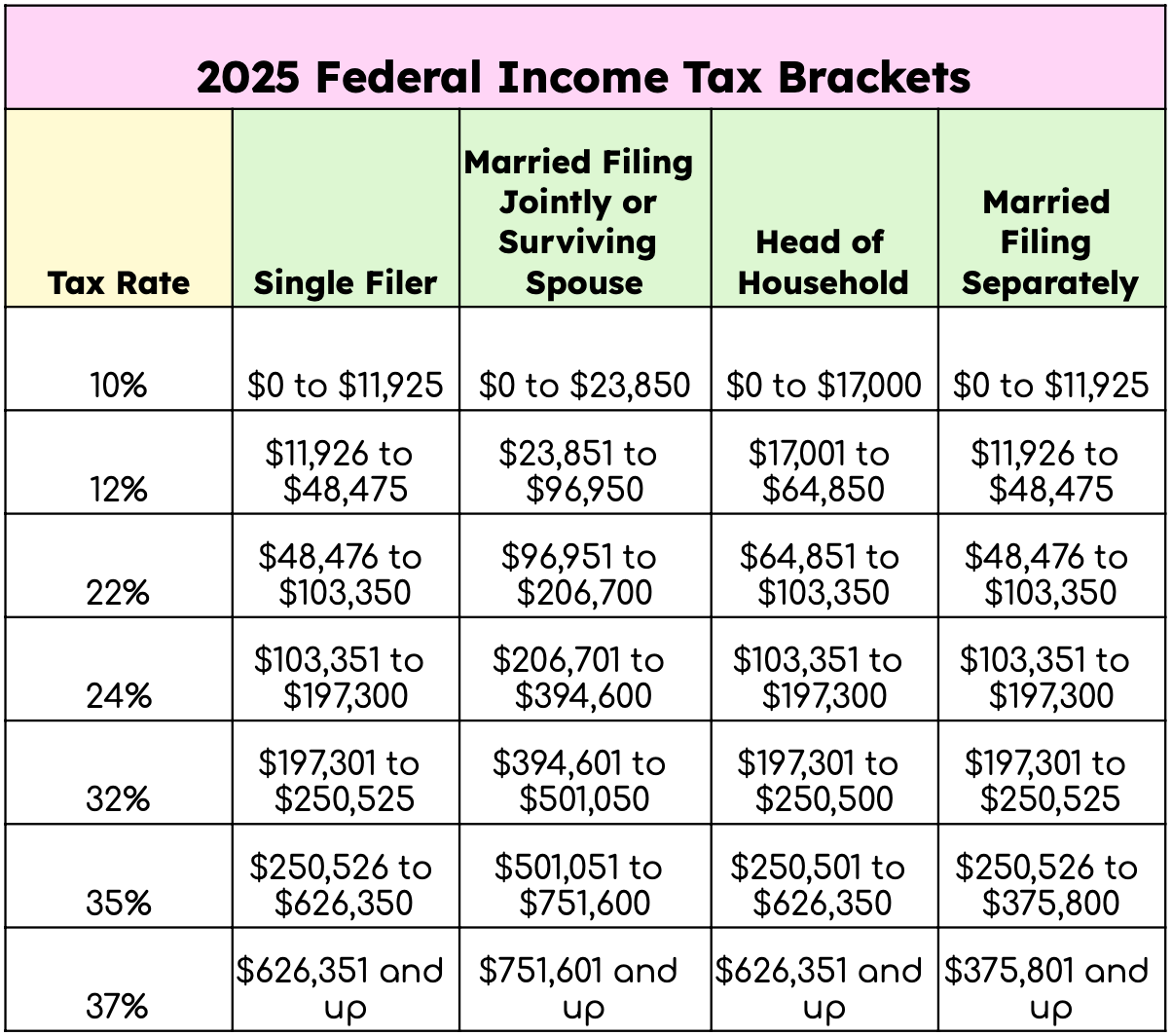

Tax brackets

Below is a table of the 2025 federal income tax brackets:

Since how to file your taxes is not something taught in school and the highest federal tax rate that applies to your income is often referred to as “your tax bracket,” it is a common misconception that there is solely one tax rate you fall into based on your income. This, however, is not the case.

Each of the tax rates listed above only apply to the income within their corresponding dollar amounts, not the entire income amount. For example, a taxpayer who is a single filer and made $60,000 of taxable income in 2025 will pay:

- 10% on the first $11,925 of their income

- .10 * $11,925 = $1,192.50 (which will be rounded up to $1,193)

- 12% on the dollars between $11,926 and $48,475

- .12 * ($48,475-$11,925) = $4,386

- 22% on the dollars between $48,476 and $60,000

- .22 * ($60,000-$48,475) = $2,525.50 (which will be rounded up to $2,526)

So the total federal income tax owed on their $60,000 of income is $8,114.

$1,193 + $4,386 + $2,536 = $8,114

Not 22% of $60,000, which would be $13,200.

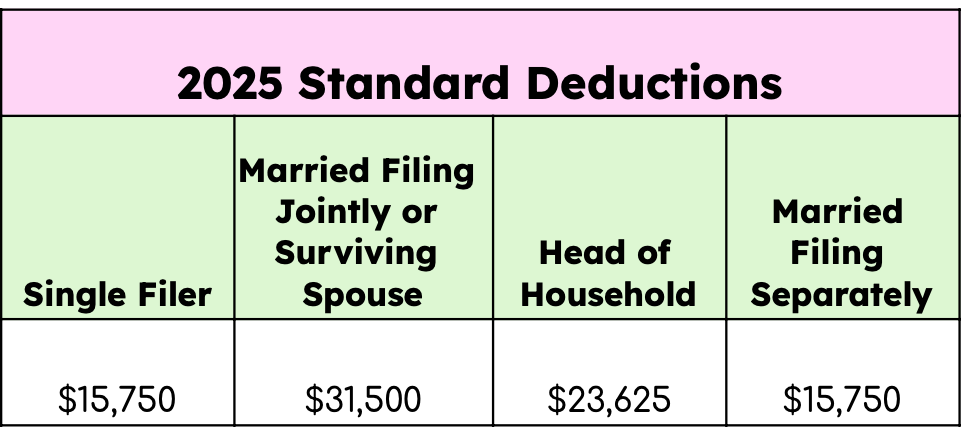

The standard deduction

To further complicate tax bracket matters, the U.S. government allows for standard deductions, i.e. the amount of income you can exclude from taxes before federal tax rates begin to apply.

*Deduction amounts are higher if you are over the age of 65 or blind

If our imaginary taxpayer who is a single filer and made $60,000 of taxable income in 2025 takes the standard deduction of $15,750, this means their $60,000 will be viewed as $44,250. With this, they’ll no longer be in the 22% tax bracket because it starts at $48,476.

Instead, they would owe:

- 10% on $11,925 of their income

- .10 * $11,925 = $1,192.50 (which will be rounded up to $1,193)

- 12% on the dollars between $11,926 and $44,250

- .12 * ($44,250-$11,925) = $3,879

- .12 * ($44,250-$11,925) = $3,879

So thanks to the standard deduction, their $60,000 of income will be treated as $44,250 and the federal income tax owed on it is $5,072.

$1,193 + $3,879 = $5,072

As for other ways to lower their 2025 income that is subject to federal taxes, they could’ve also maxed out their traditional 401(k) contributions (provided they have said retirement plan) to spare another $23,500 of their $60,000 from the federal income tax vacuum.

Of course, this would also mean they were able to successfully live off of $36,500 of income in 2025, less the usual amount of taxes taken out of each paycheck, so they need to have a floating box of bill coverage funds somewhere. Are we seeing how milking the tax system (and saving for retirement) requires you to have money in the first place (i.e. enough to comfortably afford to contribute to society and just pay the damn taxes)? The usual mention of the billionaire and richy-rich exploitations is capital gains and estate taxes, but may as well throw in another instance of “wealth inequality in action” to the mix.

If you’re looking for a quick way to determine your [highest] tax bracket and estimated federal income tax due, you can use the Tax Act calculator here.